This has been a year of adjustment at the government, firm, and household levels. You only need to look at the UAW strike with the big three automakers to feel what is at stake. With the Federal Reserve leaving the fed fund rate at 5.25% - 5.50% after 11 hikes with seven consecutive rate increases as of March 2022, these entities have now begun to reset their budgets.

Visibility is increasing, and it is not pretty. After Powell’s comments on September 20, 2023, there will be another rate hike or two, and rates may stay higher longer. The reality of the hikes is now beginning to take root.

Greg Ip of the Wall Street Journal1 had an insightful article where he outlined several potential headwinds. With 67% of the U.S. Treasuries maturing within the next five years at higher rates and the continued need for cash to fund our ongoing deficit (the U.S. Treasury2 projects a $1.524 trillion 2023 deficit), the federal government’s interest expense will rise in absolute terms. This year our net interest expenditure will be $663 billion, which is 16.62% of our total receipts according to the Congressional Budget Office (CBO).

In addition to the national debt being refinanced, according to Goldman Sacs, this year $600 billion of corporate debt is maturing and is expected to increase to over $1 trillion a year from 2025 to 2028. The impacts on the firms are obvious: reduced profits, lower investor returns, and the potential for downgrades, as well as declining portfolio values.

Add to this list the $1.5 trillion in commercial property debt that will come due by the end of 2025, and an increase in household credit card debt and rising interest rates. Auto loan past-due rates have been rising and millions will resume payments on student loan debt after a three-year hiatus due to the COVID pandemic.

You can begin to feel the ground shake under your feet as disposable income will take a hit across government, company, and household income statements.

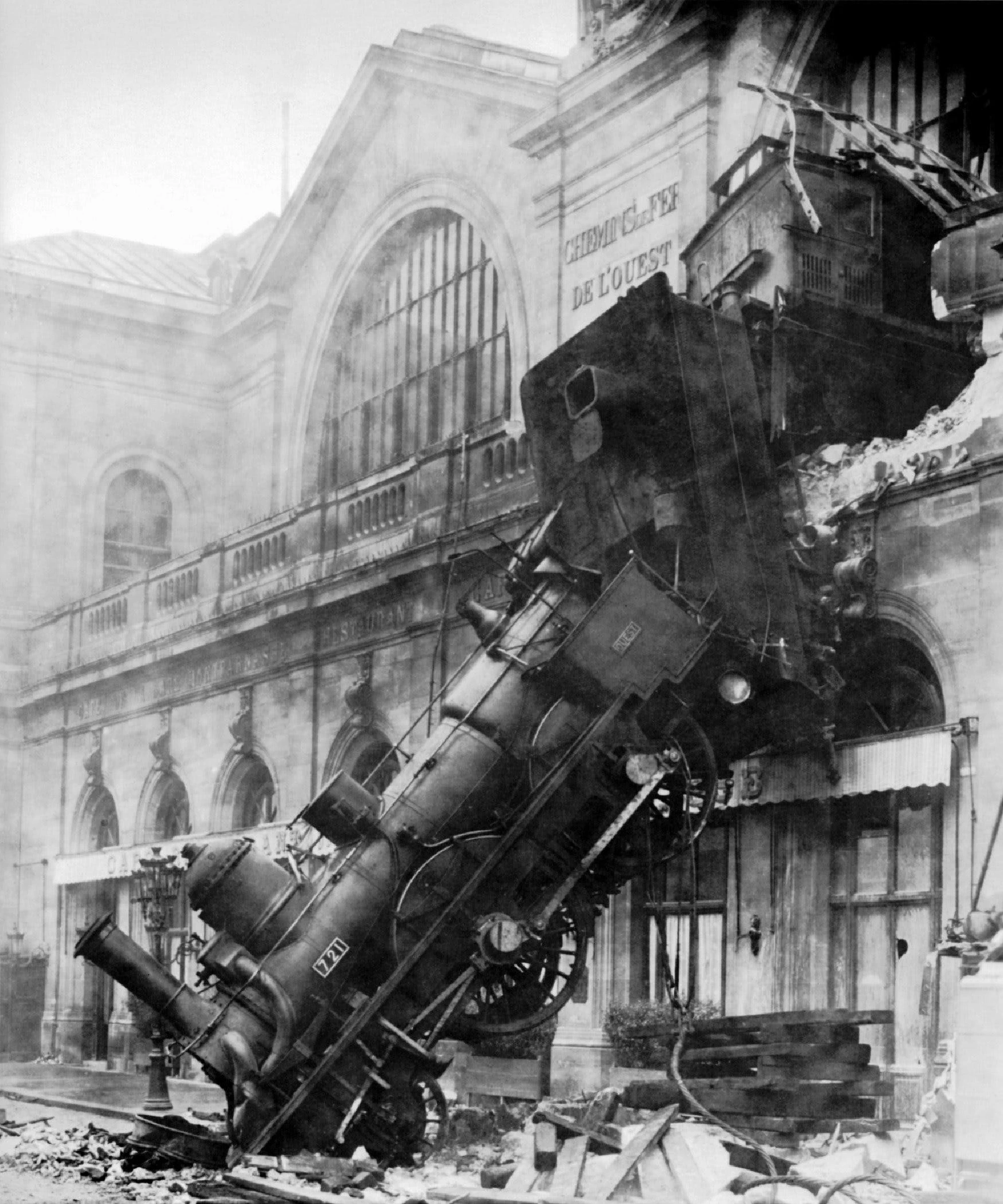

Think of two trains barreling towards each other, both fueled by declining disposable income due to a mounting increase in debt service. This analogy shows how quickly economic activity can shrink, leading to less spending.

There are areas where money is flowing to, such as here in the United States. According to the latest Treasury International Capital3 (TIC) data release by the US Department of Treasury, “the sum-total in July 2023 of all net foreign acquisitions of long-term U.S. securities, short-term U.S. securities and banking flows was a net TIC inflow of $140.6 billion.” Foreigners increased their holdings of U.S. Treasury bills by $75.8 billion. Foreign resident holdings of all dollar-denominated short-term U.S. securities and other custody liabilities increased by $85.9 billion. Many investors abroad still believe in America.

In addition, now that the bond market has begun to level off, domestic investors have returned. According to Morningstar Direct4, in the second quarter of 2023 investors withdrew $25.3 billion from equities and increased a net $72.6 billion in taxable bond funds.

What then is new in the market? Total return seems to be drawing attention to investments that may not have as much cash flow today because of rising debt costs but have promising prospects such as real estate developments, direct co-investment, and operating businesses - particularly with consumer staples. In other words, bread & butter businesses are more attractive now.

Among tax driven investments such as 1031 DST’s and Qualified Opportunity Zone Funds (QOF), Novogradac5 reported that sales in QOFs have rebounded in the second quarter of 2023 to $1.33 billion from a record low first quarter total of $681.9 million, a substantial dropped off from last year’s (2022) levels of $9.36 billion. In my view, the rising cost of capital is the main determinant as prospective buyers continue to sit on the sidelines until they can quantify their risk. For buyers who feel they have a certain level of control in pricing their product (price discovery), inflation concerns do not seem to be affecting them as much.

To state the obvious, this is a time when you really need to focus and get comfortable with your investments and to make sure you are aware of any updates or changes in the sponsors you have invested in, particularly with the credit stack.

Best Regards,

J. Carlos Martinez

Crescent Securities Group, Inc.

Greg Ip, Rates Are Up. We’re Just Starting To Feel The Heat. Wall Street Journal, September 2, 2023 undo

Treasury Direct, Monthly Treasury Statement Receipts and Outlays of the United States Government (MTS), August 23, 2023 undo

U.S. Department of The Treasury, September 18, 2023 undo

Morningstar Direct. Date as of June 30, 2023 undo

John Sciarretti, Overall QOF Equity Bounces Back in Second Quarter, but Far Behind 2022 Numbers, Novogradac August 2, 2023 undo